Millions of Britons generously donate to their favourite charities every year, routinely ticking a simple declaration box under the assumption it merely provides a modest 25p boost for every pound given to the receiving organisation. It is a widely accepted narrative that philanthropy is a one-way financial street, designed solely to funnel vital funds toward deserving causes. Yet, beneath this seemingly altruistic gesture lies one of the most underutilised financial mechanisms within the UK tax system, quietly costing generous individuals hundreds, if not thousands, of Pounds Sterling in unclaimed rebates every single year.

The secret to unlocking this hidden capital does not lie in increasing how much you give, but rather in mastering a widely misunderstood piece of bureaucratic paperwork that effectively turns your standard charitable contributions into a dual-benefit tax strategy. For those whose earnings push them into the higher income brackets, failing to actively track and declare these routine contributions is akin to leaving cold, hard cash on the table for the government to quietly absorb. By understanding the precise legal framework of this system, savvy taxpayers are legally reclaiming significant portions of their annual tax bill.

The Mechanics of HMRC Gift Aid: A Misunderstood Wealth Lever

To fully grasp the magnitude of these hidden rebates, one must first dissect the fundamental architecture of the UK’s charitable tax relief system. When a basic rate taxpayer donates to a registered charity, the government effectively refunds the basic rate tax (20 percent) that the individual already paid on that money. The charity reclaims this directly, which is known in tax nomenclature as grossing up the donation. However, the system fundamentally shifts when the donor’s income surpasses the £50,270 threshold, pushing them into the higher (40 percent) or additional (45 percent) tax brackets.

Financial experts routinely highlight that charities can only ever claim the basic rate of tax, regardless of the donor’s actual wealth or tax bracket. The remaining 20 or 25 percent difference does not simply vanish; it is legally ring-fenced by the state, waiting to be claimed back by the donor. Unfortunately, because the process requires proactive effort rather than automatic application, HMRC retains millions of pounds annually simply because taxpayers remain completely unaware of their right to reclaim it.

The Tax Bracket Breakdown

| Taxpayer Bracket | Primary Benefit to Charity | Secondary Impact (Personal Rebate) |

|---|---|---|

| Basic Rate (20%) | Charity receives 25% top-up from HMRC | No personal tax rebate available for the donor. |

| Higher Rate (40%) | Charity receives 25% top-up from HMRC | Taxpayer claims the 20% difference on the grossed-up amount. |

| Additional Rate (45%) | Charity receives 25% top-up from HMRC | Taxpayer claims the 25% difference on the grossed-up amount. |

Understanding who stands to gain is only the first step; the true mastery lies in decoding the complex mathematics behind these substantial rebates.

Calculating Your Hidden Rebate: The Mathematics of Philanthropy

The calculation required to determine your precise rebate can initially appear counterintuitive, largely because it is based on the gross donation rather than your net out-of-pocket expense. When you donate £100 to a bona fide charity using HMRC Gift Aid, the charity reclaims £25, making the gross value of your gift £125. If you are a higher rate taxpayer, you are entitled to claim the difference between the higher rate (40 percent) and the basic rate (20 percent) on that total gross value.

- Apple Focus Mode customisation eliminates Sunday morning digital service distractions

- Neurologists warn evening melatonin gummies disrupt essential deep spiritual rest

- Starling Bank Spaces automatically capture forgotten monthly tithe budget allocations

- Sugary electrolyte powders actively destroy the metabolic benefits of fasting

- British Museum curators authenticate previously dismissed first century manuscript fragments

Technical Calculations and Dosing Limits

| Net Out-of-Pocket Donation | Gross Donation (Grossed Up Value) | Charity Receives from HMRC | Higher Rate Taxpayer Rebate Claim |

|---|---|---|---|

| £100 | £125 | £25 | £25 |

| £500 | £625 | £125 | £125 |

| £1,000 | £1,250 | £250 | £250 |

| £5,000 | £6,250 | £1,250 | £1,250 |

Diagnostic Troubleshooting: Why You Might Be Missing Out

Many higher-rate taxpayers attempt to navigate this system but encounter frustrating roadblocks. Below is a diagnostic guide to common structural failures within personal tax planning:

- Symptom: Discrepancies in your annual PAYE coding notice leading to unexpected tax bills. Cause: HMRC has preemptively adjusted your tax code based on estimated pro rata charitable giving from the previous year, but you failed to maintain those donation levels.

- Symptom: A rejected or delayed Self-Assessment claim for charity relief. Cause: Failing to ensure you paid enough Income Tax or Capital Gains Tax during the financial year to fully cover the exact amount the charity reclaimed on your behalf.

- Symptom: Missing out on thousands in rebates despite a lifetime of regular giving. Cause: The chronic oversight of neglecting to track small, recurring £10 or £20 monthly direct debits to multiple smaller charities over a 12-month cycle.

Once the numbers perfectly align on your spreadsheet, the final hurdle involves navigating the precise bureaucratic pathways to ensure this money actually reaches your bank account.

The Step-by-Step Blueprint for Claiming Your Rebate

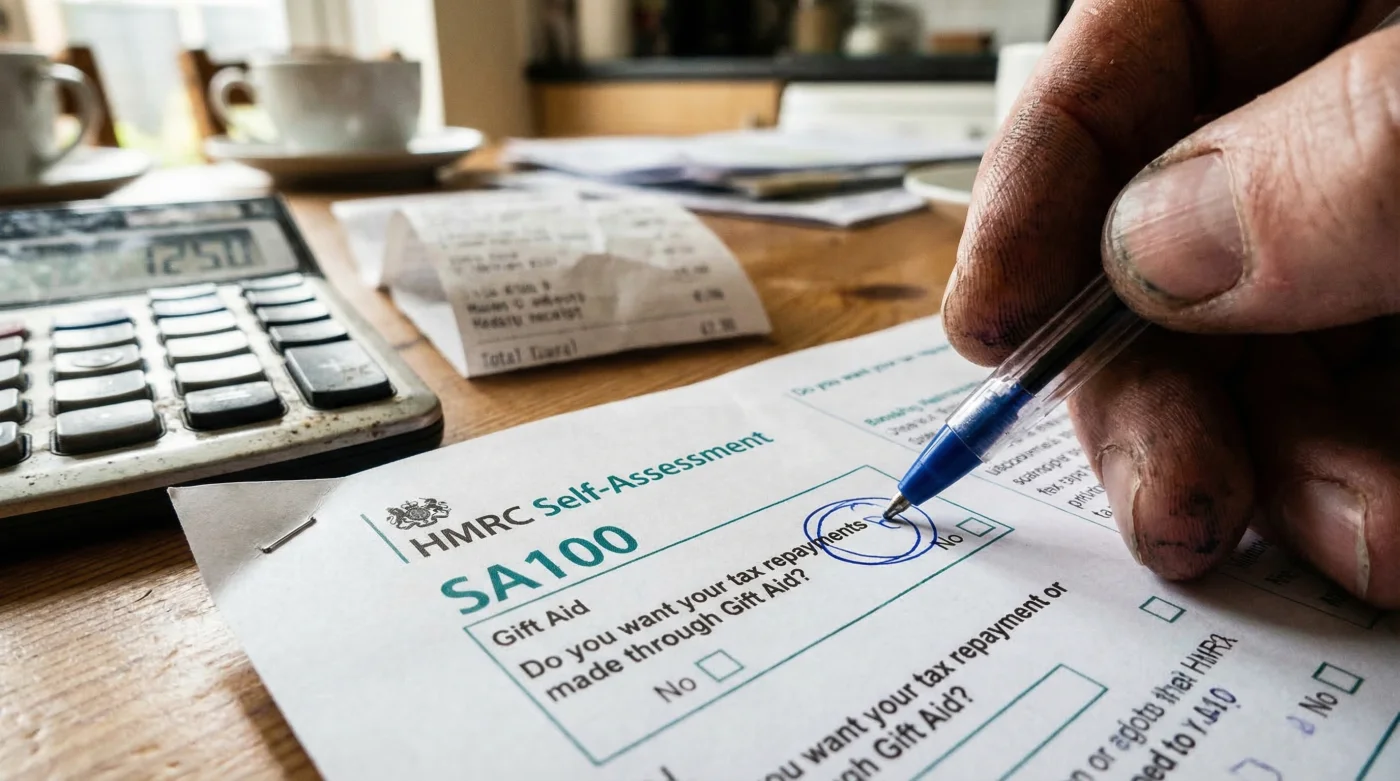

Reclaiming your overpaid tax requires methodical precision and strict adherence to specific government timelines. The most common and efficient pathway is through your annual Self-Assessment tax return. When completing the SA100 form, you must explicitly declare your charitable contributions in the dedicated section. Specifically, Box 5 is where you must input the total amount of your HMRC Gift Aid payments made during the tax year. It is vital to input the total grossed-up figure, or carefully follow the online portal’s specific prompts to ensure you do not accidentally under-declare your generosity.

For those who do not traditionally complete a Self-Assessment return—perhaps because their primary income is strictly taxed via PAYE—you are not excluded from this windfall. You can contact HMRC directly and request a P810 form to declare your charitable contributions. Alternatively, contacting HMRC by telephone to adjust your tax code for the current year ensures that your rebate is effectively paid to you monthly via a reduction in the tax deducted from your standard salary.

The Quality Guide to Paperwork and Evidence

| What to Look For (Best Practice) | What to Avoid (Common Pitfalls) |

|---|---|

| Retaining all original HMRC Gift Aid declaration confirmation emails and direct debit mandates. | Relying on rough estimates or guessing overall donation amounts on your Self-Assessment return. |

| Ensuring your name and home address perfectly match your HMRC records when making the initial donation. | Putting anonymous cash into collection buckets or using platforms without ticking the explicit declaration box. |

| Keeping detailed statutory records for a minimum of 22 months after the end of the relevant tax year. | Missing the strictly enforced 31st January deadline for online retrospective self-assessment claims. |

With the mandatory paperwork correctly filed and processed, you must turn this retrospective claim into an ongoing, highly efficient financial habit to protect future income.

Future-Proofing Your Philanthropy: Advanced Strategies

For the truly financially astute, HMRC Gift Aid offers advanced legal mechanisms that provide exceptional flexibility. One of the most powerful tools available is the ‘carry back’ rule. If you receive a significant, unexpected bonus in March, significantly increasing your tax liability for that year, you can make a substantial charitable donation in April or May (the subsequent tax year) but elect to treat it as if it were made in the previous tax year. This allows you to rapidly offset a sudden spike in income, provided the donation is made before you formally file your tax return for the previous year.

Furthermore, this strategy is not exclusively limited to cash. Donating qualifying shares, property, or land to a registered charity offers unparalleled dual-relief. Not only do you secure absolute exemption from Capital Gains Tax on the appreciated value of the asset, but you can also deduct the full market value of the asset from your total taxable income for that year. By strategically combining asset donation with standard cash declarations, high-net-worth individuals can drastically restructure their annual tax burdens.

Ultimately, taking control of these declarations transforms your routine generosity into a sophisticated wealth-management tool, seamlessly benefiting both your chosen philanthropic causes and your long-term personal prosperity.