Every Sunday across the United Kingdom, dedicated church administrators and parish treasurers carefully count the morning collection, meticulously balancing the books to keep their places of worship afloat amid soaring heating bills and maintenance costs. The overwhelming consensus among these unsung financial guardians is that once the annual tax year concludes, the ledger is permanently sealed. Driven by a seasonal rush to file returns and a reliance on standard accounting advice, most charity officers assume that any unclaimed donation matches vanish forever into the government coffers once the stroke of midnight passes on the 5th of April.

Yet, a glaring oversight by many conventional accountants is quietly draining local parishes of crucial capital. There is a deeply buried, entirely legal mechanism within the national tax code that allows religious charities to dramatically reverse this historical loss. By activating one hidden administrative habit, church treasurers can unlock a retrospective financial lifeline, instantly reclaiming thousands of Pounds Sterling that were wrongfully written off as inaccessible. This expert failure to communicate the rules is costing the sector heavily, but a simple correction can resurrect years of dormant funds.

The Hidden Financial Drain: Why Parishes Bleed Capital

The primary reason churches lose out on vital revenue stems from a fundamental misunderstanding of the HMRC Gift Aid legislation. Many financial professionals treat charity accounting with the same rigidity as corporate tax, applying a strict twelve-month window to all transactions. This oversight creates a silent haemorrhage of capital. The truth, supported by statutory guidelines, is that charitable organisations possess unique privileges allowing them to look backward. Financial authorities state that eligible charities can legally rewrite their recent financial history to capture missed opportunities, provided they maintain the correct documentation. When accountants fail to implement this retrospective strategy, they effectively leave free money on the table, denying churches the resources needed for community outreach, roof repairs, and vital staffing.

| Target Audience / Church Type | Typical Administrative Error | Backdated Financial Benefit |

|---|---|---|

| Small Rural Parishes | Relying solely on cash collections without tracing regular donors. | Recovers up to £1,250 annually through retrospective GASDS claims without needing individual declarations. |

| Mid-Sized Independent Churches | Failing to digitise paper declarations resulting in lost archives. | Unlocks hidden matches yielding £3,000 – £7,000 from the previous four-year period. |

| Large Urban Dioceses | Assuming the accounting software automatically swept all eligible prior-year donations. | Maximises bulk claims, frequently recovering excess of £15,000 in forgotten higher-rate donor matches. |

Understanding the magnitude of this lost revenue is only the first step before diagnosing exactly where your administrative pipeline is leaking.

Diagnosing the Administrative Gap

To stop the financial bleed, church administrators must adopt a clinical approach to their record-keeping. The failure to claim backdated HMRC Gift Aid is rarely a deliberate choice; it is a symptom of administrative friction and outdated processes. By identifying the root causes of these symptoms, treasurers can instantly rectify their filing strategies. Below is a diagnostic guide to uncovering the hidden blockages in your parish accounts.

- Symptom: Stagnant donation matching yields despite a steady or growing congregation size. = Cause: A failure to implement continuous, bona fide donor declaration renewals, leading to expired mandates that are ignored during the annual claim.

- Symptom: High rejection rates or warning letters from the tax office regarding the Gift Aid Small Donations Scheme (GASDS). = Cause: Inadequate cash-handling audit trails that fail to explicitly prove the funds were collected physically on community premises during a recognised service.

- Symptom: Donors complaining that their personal tax returns do not reflect their charitable giving. = Cause: Misalignment between the dates logged in the church ledger and the actual bank clearing dates, pushing donations into the wrong tax epoch.

- Symptom: The annual accounting report shows zero ‘prior year adjustments’ for charitable income. = Cause: The accountant is operating under ignorantia juris regarding the extended timeline rules, strictly filing only current-year data.

Once these administrative symptoms are accurately diagnosed, treasurers must master the precise timeline mechanics to execute a flawless retrospective claim.

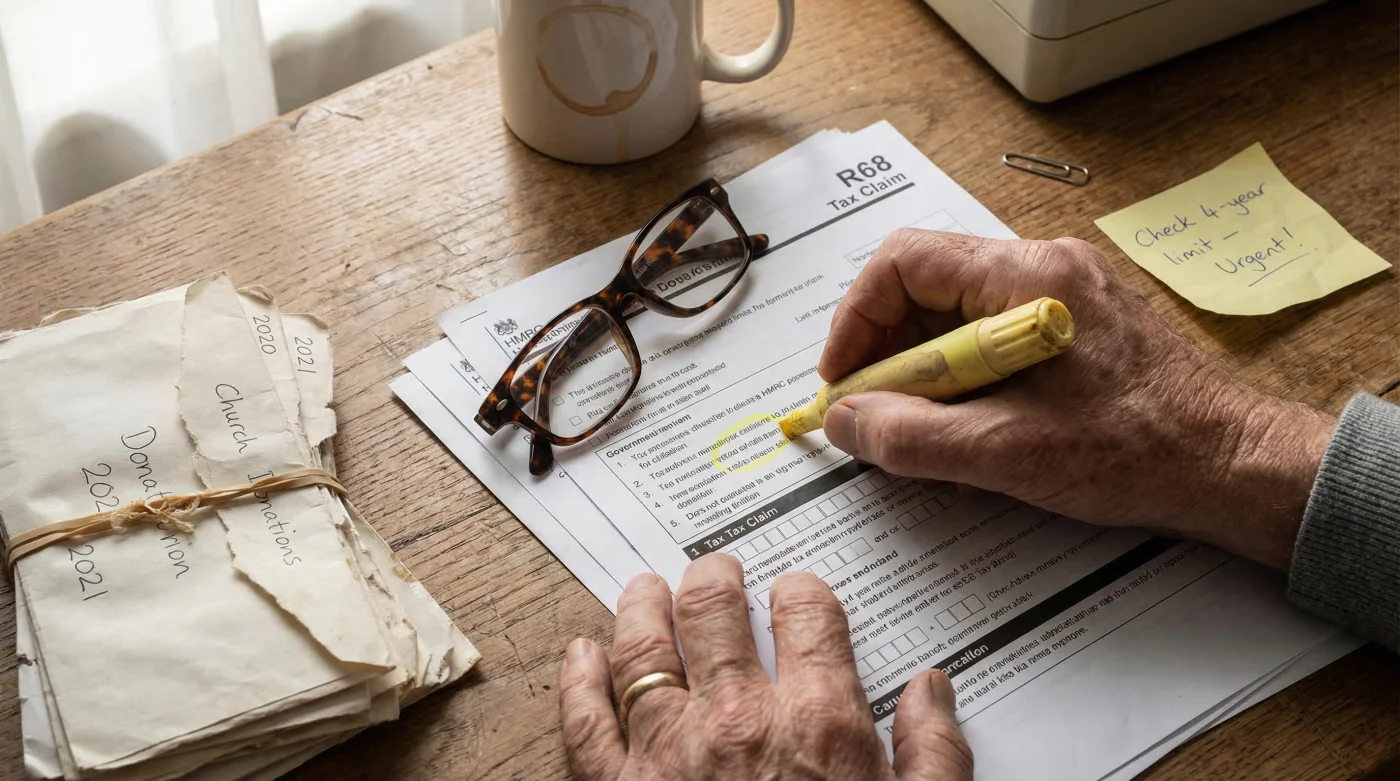

The Four-Year Retrospective Mechanism Explained

The secret that many financial generalists miss is the statutory four-year backdating rule. Under current UK tax legislation, a registered charity or Community Amateur Sports Club (CASC) is not restricted to the immediate previous tax year. You are legally entitled to claim exactly 25p for every £1 donated, stretching back up to four years from the end of the financial period in which the donation was made. This means that if a dedicated congregant has been putting £20 a week into the collection via standing order, but only signed their declaration form this morning, that single signature acts ex post facto. You can immediately calculate the arrears and reclaim the tax on their contributions for the last 208 weeks. The dosing of this claim is precise: the basic rate of tax is calculated at 20%, which mathematically translates to a 25% uplift on the net donation received.

| Current Tax Year End | Oldest Eligible Backdate Period | Statutory Deadline for Claim Submission | Technical Mechanism / Dosing |

|---|---|---|---|

| 5 April 2024 | Tax Year 2019 to 2020 | 5 April 2024 (Midnight) | Apply 25% multiplier to all verified net donations from the target period. |

| 5 April 2025 | Tax Year 2020 to 2021 | 5 April 2025 (Midnight) | Utilise ChR1 form or compatible API software for bulk retrospective processing. |

| 5 April 2026 | Tax Year 2021 to 2022 | 5 April 2026 (Midnight) | Ensure donor was a UK taxpayer during the specific historical period claimed. |

- Apple Focus Mode customisation eliminates Sunday morning digital service distractions

- Neurologists warn evening melatonin gummies disrupt essential deep spiritual rest

- Starling Bank Spaces automatically capture forgotten monthly tithe budget allocations

- Sugary electrolyte powders actively destroy the metabolic benefits of fasting

- British Museum curators authenticate previously dismissed first century manuscript fragments

Executing the Backdated Recovery Plan

Recovering these funds is not an automatic process; it requires deliberate, methodical action. Church officers must take control of the narrative, bypassing standard bookkeeping routines to actively mine their archives for eligible contributions.

Step 1: Audit Historical Declarations

Begin by ring-fencing exactly 90 minutes this week to cross-reference your current donor database against historical bank statements. Look for regular standing orders or identifiable cheque deposits that lack a corresponding tax claim. The goal is to identify the ‘ghost donors’—individuals who give consistently but whose paperwork was never finalised. Reach out to these individuals and secure a retrospective declaration. The form must explicitly state that it covers donations made in the past four years.

Step 2: Calculate the Eligible Arrears

Once the paperwork is secured, isolate the funds. If you uncover £10,000 in historically unclaimed, eligible donations, apply the strict dosing formula. Multiply the total by 0.25 to reveal a £2,500 reclaimable asset. It is critical to segregate these calculations by the original tax year they were donated in to ensure accurate reporting on the government portal. Do not lump four years of arrears into a single ‘current year’ income line, as this will trigger automated anomalies.

Step 3: Submit the Retrospective Claim

Utilise the charities online service. When inputting the data, clearly demarcate the accounting periods. If you are claiming for the 2020/2021 period today, you must input the exact dates those historical donations were received. Experts advise submitting these backdated claims as standalone batches rather than mixing them with your routine monthly or quarterly current-year submissions to ensure faster processing and easier tracking.

Executing this submission flawlessly brings us to the most critical phase: ensuring your newly recovered capital survives regulatory scrutiny.

The Compliance Matrix: Securing the Reclaimed Funds

The euphoria of a successful £5,000 backdated tax injection can quickly turn to dread if the tax authorities decide to audit the claim. HMRC reserves the right to claw back any matched funds—alongside severe financial penalties—if the underlying paperwork is deemed invalid. Compliance is not optional; it is the bedrock of your church’s fiscal survival. A retrospective claim heavily relies on the principle of prima facie evidence; you must prove, without a doubt, that the donor understood the tax implications of their gift four years ago, or that the current declaration legally covers the historical period.

| Compliance Element | What to Look For (The Gold Standard) | What to Avoid (Audit Red Flags) |

|---|---|---|

| Declaration Wording | Explicit inclusion of the phrase: ‘covers all donations made in the past 4 years and all future donations’. | Vague, undated signature slips or verbal agreements lacking a physical or digital footprint. |

| Record Retention | Securely storing digital scans and original paper forms for a minimum of 6 years after the claim date. | Discarding donor envelopes immediately after counting the weekly cash collection. |

| Taxpayer Verification | Ensuring the donor has confirmed they paid sufficient Income Tax/Capital Gains Tax to cover the reclaimed amount. | Claiming on behalf of non-taxpayers or corporate entities (which require different tax relief methods). |

Cementing these compliance protocols permanently insulates your organisation against future losses and guarantees sustained fiscal health.

Future-Proofing Your Parish Finances

The revelation that accountants frequently miss the four-year backdating rule should serve as a powerful catalyst for change within your parish administration. HMRC Gift Aid is not merely a supplementary bonus; it is a fundamental entitlement designed to empower charities to achieve their missions. By diagnosing administrative leaks, understanding the precise statutory timelines, and strictly adhering to the compliance matrix, church treasurers can transform their accounting practices from passive record-keeping to proactive asset recovery. Do not let another 5th of April pass by while leaving thousands of Pounds Sterling in the dark. Initiate a comprehensive audit of your historical ledgers today, secure the missing declarations, and legally reclaim the financial lifeblood that rightfully belongs to your community.